No products in the cart.

Why Your Premium Credit Card Perks Are Disappearing

Discover how rising costs and bank regulations are devaluing premium credit card perks, impacting your wallet and spending behavior.

“`html

The Great Perks Disappearing Act

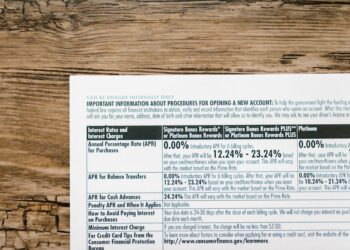

For years, premium credit cards offered perks like lounge access, travel insurance, concierge services, and points for first-class flights. The deal was simple: pay a high annual fee, and enjoy benefits that most could only dream of. However, as banks face rising funding costs, stricter regulations, and slowing consumer spending, these perks are disappearing.

Recent data shows that bank profitability has declined due to rising interest rates, inflation-related wage pressures, and slower loan growth. In the U.S. and abroad, banks that relied on premium card fees to fund lavish perks now see those fees shrinking due to higher capital requirements and a shift toward lower-margin products.

This has led to a quiet but significant change. Where premium cards once included travel credits, lounge passes, and complimentary upgrades, many issuers are now cutting annual travel credits, limiting lounge visits, and reducing insurance coverage. These changes are often hidden in fine print under the guise of “product optimization.”

Why Banks Are Pulling Back on Benefits

Rising Costs and Regulatory Pressure

Maintaining premium card rewards is costly. For example, travel insurance costs rise with global airline pricing and healthcare premiums. Concierge services require dedicated staff, whose salaries have outpaced inflation. As banks faced pressure on earnings, they scrutinized expenses, and the rewards budget was one of the first to be cut.

Why Banks Are Pulling Back on Benefits Rising Costs and Regulatory Pressure Maintaining premium card rewards is costly.

Industry surveys indicate many banks plan to reduce premium card benefits soon, citing rising costs and regulatory pressures. This shift is not just a reaction to market conditions but a strategic change driven by ongoing challenges.

The Unsustainable Cost of Perks

The cost of perks has become unpredictable. Travel insurance claims surged after geopolitical disruptions, and lounge access fees increased as airport operators renegotiated contracts. Concierge services have expanded, requiring technology and 24-hour staffing, raising operational costs beyond typical credit card margins.

In response, banks are cutting the most expensive perks first. Annual travel credits are reduced, lounge access is capped, and many insurers are limiting complimentary coverage to basic fraud protection, which is now a regulatory minimum.

What This Means for Consumers and Their Wallets

Shifting Loyalty and Rising Fees

You may also like

AI & Technology

AI & TechnologyNvidia to Invest $1 Bil in Naver, SpaceX Starship Launch, More

Nvidia's $1 billion investment in Naver aims to enhance AI capabilities and expand influence in the global market, creating opportunities for software engineers and reshaping…

Read More →For cardholders, reduced benefits mean a tough cost-benefit analysis. Many consumers would consider switching cards if their perks were cut. Some users might accept higher annual fees for better rewards, but only if the value is clear.

As banks cut benefits, they are also raising fees. Some have increased annual fees for the same card tier, while others are bundling previously free services, like basic travel insurance, into paid add-ons. This could lead to higher costs for premium cardholders, even as perceived value declines.

Impact on Spending Behaviour

Research shows many consumers use credit cards mainly for rewards and would switch cards if those rewards changed. As the appeal of points and travel credits fades, the incentive to spend on high-margin categories weakens.

As banks cut benefits, they are also raising fees.

Early signs indicate a slight decline in travel spending among premium cardholders. Hospitality operators report fewer bookings and increased price sensitivity. If generous travel credits disappear, consumers may rethink splurging on trips, potentially hurting travel sector revenue.

Navigating the New Rewards Landscape

Consumers have options. New rewards platforms are emerging that aggregate points across multiple issuers, helping cardholders maximize remaining benefits. Additionally, “no-fee” premium cards are appearing, offering fewer perks without an annual charge.

Financial planners advise clients to view premium card benefits as variable expenses. By evaluating the value of lounge passes, insurance, and concierge services, individuals can decide if the remaining perks justify the fee or if a lower-tier card with a modest fee and cash-back rewards is a better choice.

Strategic Outlook for Banks

The reduction in lavish perks reflects a broader strategic shift. Banks are diversifying revenue streams beyond fee-heavy credit products, focusing on digital banking, wealth management, and partnerships. The premium card model is evolving into a leaner, data-driven offering that emphasizes core benefits like fraud protection and basic points accrual, while outsourcing additional services.

Regulatory changes are also influencing this shift. Increased transparency in fee structures and stricter capital rules mean banks can no longer obscure the true cost of rewards. The era of “free” premium perks is likely giving way to a more straightforward, though less glamorous, value proposition.

You may also like

Government & Policy

Government & PolicyIndia’s policy on urea | Explained

India's Cabinet Committee on Economic Affairs approved the National Investment Policy for Urea (NIPU)-2026 to enhance self-reliance in urea production amid rising demand and climate…

Read More →Banks are diversifying revenue streams beyond fee-heavy credit products, focusing on digital banking, wealth management, and partnerships.

Looking Ahead: The New Currency of Cardholder Value

The premium card market is moving away from excess, forcing consumers to reassess the true value of their benefits. As banks tighten budgets and regulators demand clarity, the future of credit card rewards will focus on tangible, measurable value rather than flashy perks.

“`